Retirement planning involves a detailed consideration of factors like when to start receiving Social Security benefits. A worker can choose to retire as early as age 62, but doing so may result in a benefits reduction of as much as 30 percent.

While the opportunity to claim benefits early exists, it comes with important implications that individuals should fully understand before making a decision.

A. Eligibility Age for Early Retirement

- You can start claiming Social Security benefits as early as age 62.

B. Reduction in Benefits

- If you claim Social Security benefits before reaching your full retirement age (FRA), your monthly benefit amount will be reduced. Full retirement age is between 66 and 67, depending on your birth year.

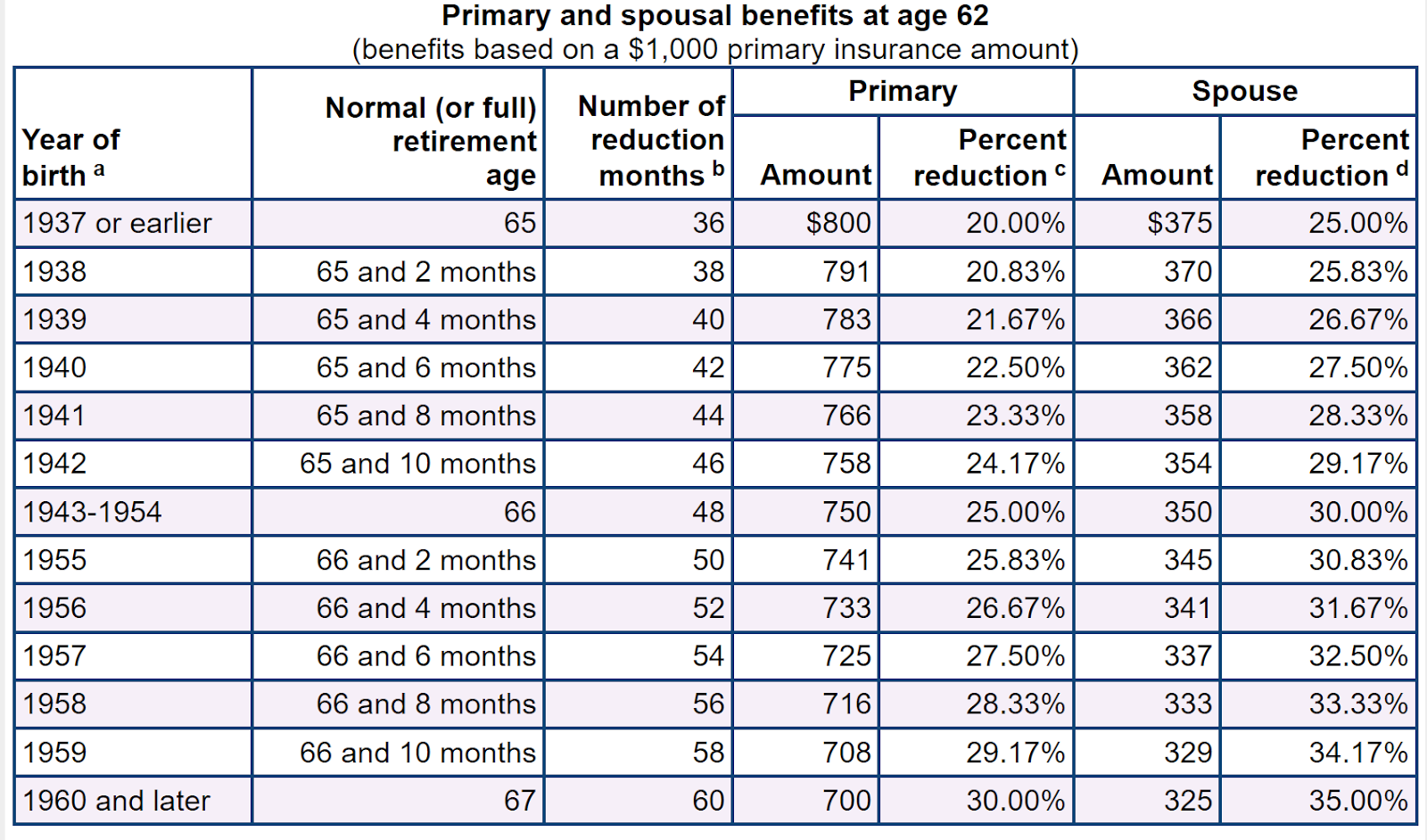

Reduction Example:- If your full retirement age is 66 and you start benefits at 62, your benefits could be reduced by about 25-30%.

- The reduction is permanent and will affect your monthly benefit amount for the rest of your life.

C. Full Retirement Age (FRA)

- For those born between 1943 and 1954, FRA is 66.

- For those born in 1960 or later, FRA is 67.

- For those born between 1955 and 1959, FRA is between 66 and 67, depending on the year.

D. Earnings Limit

- If you start receiving Social Security benefits before your FRA and continue to work, your benefits could be temporarily reduced if you earn over a certain limit.

Earnings Limit for 2024:- If you’re under FRA for the entire year, $21,240 is the limit. Earnings above this limit will reduce your benefits by $1 for every $2 earned over the limit.

- In the year you reach FRA, a higher limit applies ($56,520 for 2024), and your benefits are reduced by $1 for every $3 earned over the limit until the month you reach FRA.

E. Planning Considerations

- Deciding when to claim Social Security depends on various factors including your health, life expectancy, financial needs, and whether you plan to continue working.

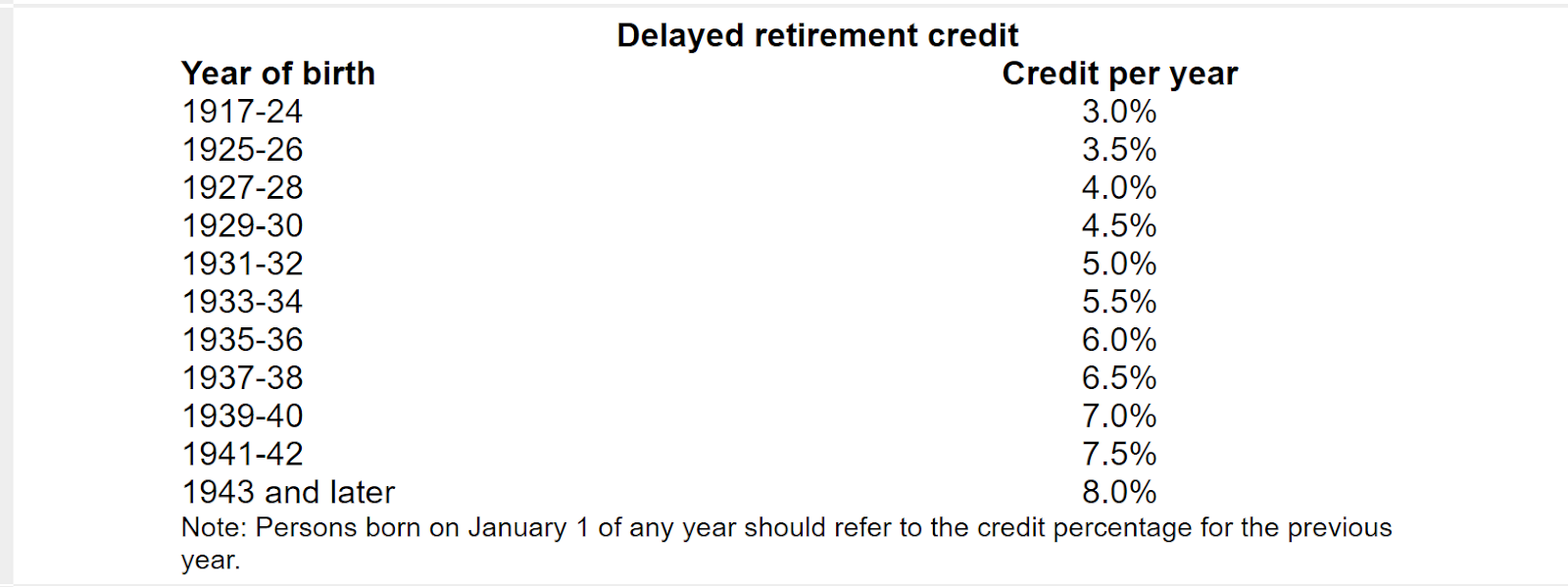

- Delaying benefits past your FRA can increase your monthly benefit. For each year you delay past FRA, up to age 70, your benefit can increase by about 8% annually

F. Delay Your Social Security benefits

- If you decide to retire early, you have the option of delaying your Social Security benefits. However, you’ll need to consider how to fund your lifestyle from other sources until you start claiming Social Security.

- This strategy may work particularly well for married couples because they have more flexibility in how they claim benefits. For example, one spouse can start claiming their Social Security benefits early, providing an income stream, while the other spouse delays their benefits to maximize the eventual payout.

Early Retirement Reduces Benefits

A. Age Eligibility:

- Social Security provides individuals with the option to claim retirement benefits as early as age 62.

- Your Full Retirement Age (FRA) is determined by your birth year and plays a crucial role in deciding the full benefit amount you are entitled to.

B. Reduced Benefits:

- Opting to claim benefits before reaching your FRA results in a permanent reduction in your monthly benefit amount.

- This reduction can be substantial, potentially reaching up to 30% when benefits are claimed at 62 with an FRA of 67.

C. The Cumulative Lifetime Benefits May be Lower:

Commencing benefits early leads to an increase in the number of monthly payments you receive, albeit at a reduced amount per payment.

While the immediate benefit lies in more frequent payments, the cumulative lifetime benefits may be lower, especially for individuals with longer lifespans. This is because individuals with longer life spans will receive benefits for more years. If they claim early and face reduced monthly payments, the lower payments will accumulate over a longer period, potentially resulting in a lower total benefit compared to if they had waited until FRA or beyond for higher payments.

This might seem unfair, but the Social Security system is designed to balance benefits based on the assumption that some people will claim early and others will delay. The idea is to provide options for different financial needs and life situations.

For those who claim early, the system offers immediate income, which can be crucial if someone has pressing financial needs or health issues. Conversely, delaying benefits can result in higher monthly payments, which can be beneficial for those who live longer.

The system aims to offer flexibility while managing overall benefit payouts in a way that accounts for various individual circumstances.

Delayed Retirement Increases Benefits

By retiring early, you could miss the chance to increase your Social Security benefits through delayed retirement credits. Social Security raises your monthly benefit for each month you delay claiming after your full retirement age, up to age 70. For instance, if your full retirement age is 67 and you wait three years to claim, your benefit could reach 124% of the full amount.

The table below from the Social Security Administration shows the annual increase rate based on your birth year.

Calculate How Much You’ll Get from Social Security

If you’re curious about your Social Security benefits, you can use calculators to get an estimate. Tools like SmartAsset Social Security Calculator and the Social Security Administration’s (SSA) official calculator can help. These tools estimate your potential earnings based on factors like your annual income, birth year, and the age at which you start receiving benefits.

Social Security benefits are calculated using your highest 35 years of earnings, which the SSA uses to determine your average monthly indexed earnings (AIME). If you retire early, before working for at least 35 years, you might receive lower Social Security benefits—one of the potential downsides of early retirement.

Effects of Early retirement for Spouses

If an individual claims benefits before reaching their Full Retirement Age, the reduced benefit amount can impact the spousal benefits available to their partner.

Spousal benefits are typically a percentage of the primary earner’s benefit amount and are adjusted based on the claiming strategy of the primary beneficiary. The spousal benefit can be up to half of the worker’s primary insurance amount, depending on the spouse’s age at retirement. If the spouse begins receiving benefits before their full retirement age, the spousal benefit will be reduced. This may result in receiving as little as 32.5% of the worker’s primary insurance amount depending on the retirement age. However, if a spouse is caring for a qualifying child, the spousal benefit is not reduced.

If a spouse is eligible for a retirement benefit based on their own earnings and that benefit is higher than the spousal benefit, they will receive their own retirement benefit. Otherwise, they will receive the spousal benefit.

Let’s look at this chart again:

Survivor Benefits:

Early retirement and claiming benefits prior to Full Retirement Age also have implications for survivor benefits.

- If the primary earner passes away and the surviving spouse is eligible for survivor benefits, the amount they receive may be influenced by the early claiming decisions made by the primary earner.

- The reduction in benefits resulting from early claiming can impact the survivor’s benefit amount, potentially affecting their financial security in the long term.

What If I Want to Work in Retirement?

Continued employment while receiving Social Security benefits can have implications on the amount of benefits received.

The earnings test dictates how earned income affects benefit amounts, with benefits being temporarily reduced if earnings exceed a certain threshold.

A.Overview:

- Early beneficiaries who choose to continue working while receiving Social Security benefits might face reductions if their earnings surpass a specified threshold.

- The earnings test is a mechanism to regulate the amount of benefits withheld based on the individual’s level of earned income.

B.Earnings Limit for 2024:

- In 2024, the earnings limit stands at $21,240 for individuals claiming benefits before their Full Retirement Age.

- If an individual’s earnings exceed this threshold, benefits are withheld at a rate of $1 for every $2 earned beyond the limit.

C.Impact on Benefits:

- Exceeding the earnings limit may result in a reduction of Social Security benefits to account for the additional income earned through employment.

- Once an individual reaches their Full Retirement Age, the earnings test no longer applies, and they can earn any amount without impacting their benefits.

Decision-Making Factors

Retiring early and claiming Social Security benefits can significantly impact an individual’s financial well-being in retirement. When considering early retirement, several factors come into play that can influence the decision-making process. Here, we explore key considerations individuals should take into account when evaluating whether to claim benefits before their full retirement age.

A. Financial Need:

Immediate Income:

- Individuals facing immediate financial obligations or a lack of other retirement income sources may find early benefit claiming necessary to address pressing financial needs.

- The availability of Social Security benefits can offer crucial financial support to cover essential expenses during early retirement.

B. Longevity and Health Factors:

Longevity and health factors can significantly influence the decision to claim Social Security benefits early. Here’s why:

- Health Concerns: If an individual has health issues or a shorter life expectancy, claiming benefits early can provide a steady income sooner, which might be beneficial given their uncertain lifespan.

- Family Longevity: If a person’s family has a history of shorter lifespans, they might consider claiming benefits early to ensure they can make the most of their benefits, rather than risking a delay that could result in reduced opportunities to enjoy them if health concerns arise.

Claiming benefits early can be advantageous for those who prioritize immediate financial support over maximizing long-term payouts.

C. Other Income Sources:

Evaluating additional retirement income sources like savings or other investments is crucial when deciding on early benefit claiming. Determining the sufficiency of these income streams can help individuals gauge the need and timing for claiming Social Security benefits.

D. Balancing Income and Benefits:

- Individuals considering early retirement must carefully weigh the impact of the earnings test on their benefits against the benefits of continued employment and additional income.

- Understanding how early claiming affects spousal and survivor benefits can help in developing a comprehensive retirement planning strategy.

E. Balancing Immediate Needs with Future Security:

Early claiming offers immediate financial relief but may result in a trade-off between short-term support and long-term financial security.

Claiming benefits early should be based on a holistic evaluation of retirement plans. Consideration of supplementary income sources, future healthcare needs, and other financial obligations is vital in determining the optimal claiming strategy. Creating a comprehensive financial plan that accounts for both immediate needs and future goals can help strike a balance.

Conclusion

Choosing when to claim Social Security benefits during early retirement involves a nuanced understanding of the trade-offs. While early claiming provides immediate income, it comes with permanent benefit reductions that affect lifetime income. Assessing personal circumstances, financial needs, health, and employment intentions can help make an informed decision that aligns with your retirement goals.

WeFIRE Newsletter

A weekly roundup of money news, budgeting hacks, tax strategies, book reviews, and bursts of inspiration to support you on your path to financial independence.

Y H