Imagine sipping cocktails on a tropical beach, golfing on world-class courses, or simply spending quality time with loved ones without the worry of financial constraints. While retirement might seem like a distant dream, the truth is that the earlier you start planning, the sooner you can turn that dream into reality. In fact, your 20s are the ideal time to lay the groundwork for a comfortable and fulfilling retirement.

Why so early, you ask? The power of compound interest, the ability to weather unexpected financial storms, and the opportunity to achieve true financial freedom are just a few reasons why starting your retirement plan in your 20s is a game-changer. By investing early and consistently, you can harness the magic of compound interest, where your money grows exponentially over time. Think of it as a snowball effect for your savings – a small amount invested now can turn into a substantial nest egg by the time you retire.

In this comprehensive guide, we will walk you through the essential steps to create a solid retirement plan in your 20s. From understanding your financial situation and exploring various retirement savings options to overcoming common obstacles and debunking myths, we’ve got you covered. Whether you’re a recent graduate, a young professional, or simply someone looking to take control of their financial future, this article will equip you with the knowledge and tools you need to secure a comfortable retirement and achieve your long-term financial goals.

1. Why Start Planning for Retirement in Your 20s?

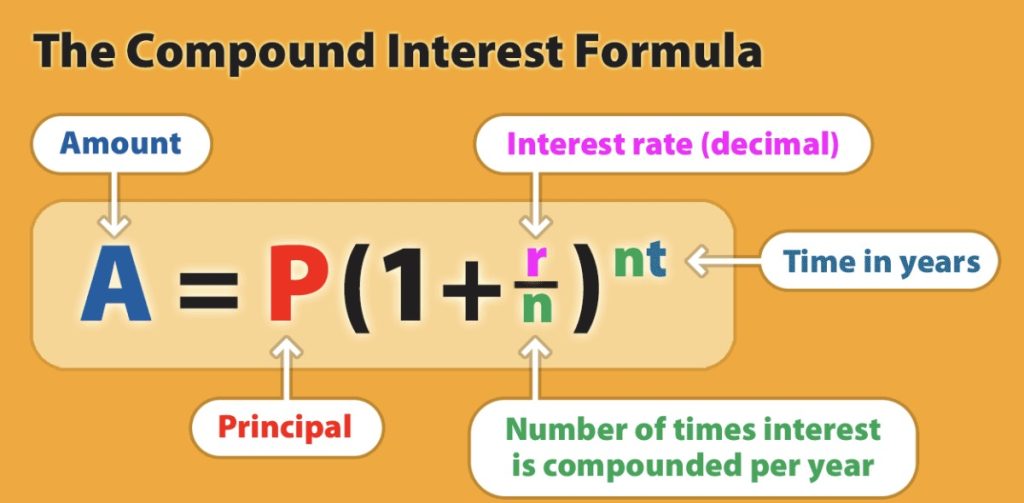

The Power of Time: Unleashing the Magic of Compound Interest

One of the most compelling reasons to start planning for retirement in your 20s is the incredible power of compound interest. This financial phenomenon allows your investments to grow exponentially over time, as the interest earned on your initial investment is reinvested, generating even more interest. The earlier you start investing, the longer your money has to compound, resulting in a significantly larger nest egg by the time you retire.

To illustrate this, let’s consider two individuals:

- Early Bird: Starts investing $5,000 annually at age 25, earning a 7% average annual return.

- Late Bloomer: Starts investing $5,000 annually at age 35, also earning a 7% average annual return.

By the time they both reach 65, the Early Bird will have accumulated over $1.2 million, while the Late Bloomer will have just over $600,000. That’s a difference of over $600,000, simply because the Early Bird started investing ten years earlier! This example clearly demonstrates the immense potential of compound interest and the importance of starting your retirement savings journey as early as possible.

Navigating Future Uncertainties: Preparing for Inflation, Career Changes, and More

Life is full of uncertainties, and your financial future is no exception. Inflation can erode the purchasing power of your savings over time, while unexpected career changes or economic downturns can disrupt your income and financial stability. By planning for retirement in your 20s, you can build a financial cushion to protect yourself from these uncertainties.

Starting early allows you to spread your savings over a longer period, making it easier to adjust to unexpected events and maintain a consistent savings plan. Additionally, early retirement planning can help you develop financial discipline and healthy money habits that will serve you well throughout your life.

Achieving Financial Freedom: Pursue Your Dreams and Retire Early

Early retirement planning isn’t just about securing a comfortable retirement; it’s also about achieving financial freedom and the flexibility to pursue your passions and dreams. By saving diligently in your 20s, you can create a financial safety net that allows you to take calculated risks, explore new career paths, or even retire early if that’s your goal.

Financial freedom gives you the power to make choices based on your values and aspirations, rather than being solely driven by financial necessity. It opens up a world of possibilities, allowing you to live life on your own terms and pursue the things that truly matter to you.

2.Understanding Your Financial Situation

Before you can embark on your retirement planning journey, it’s crucial to have a clear understanding of your current financial situation. This involves taking a close look at your income, expenses, debts, assets, and financial goals.

Income and Expense Analysis: Tracking Your Cash Flow

The first step is to track your income and expenses meticulously. Keep a detailed record of all your income sources, including salary, bonuses, side hustles, and any other sources of revenue. Similarly, track all your expenses, categorizing them into fixed expenses (rent, utilities, debt payments) and variable expenses (groceries, entertainment, dining out).

By analyzing your income and expenses, you can identify areas where you can potentially cut back and free up more money for retirement savings. Look for recurring expenses that can be reduced or eliminated, such as subscriptions you no longer use or dining out habits that can be curbed.

Budgeting: Creating a Roadmap for Your Financial Future

Once you have a clear picture of your income and expenses, it’s time to create a budget. A budget is a financial roadmap that helps you allocate your income towards your various financial goals, including retirement savings. It ensures that you’re living within your means and saving enough to secure your future.

When creating a budget, prioritize your retirement savings by setting aside a specific percentage of your income each month. A good starting point is to aim for saving at least 15% of your pre-tax income for retirement. However, you can adjust this percentage based on your individual circumstances and financial goals.

Debt Management: Tackling High-Interest Debt

High-interest debt, such as credit card debt or personal loans, can be a major obstacle to your retirement savings goals. The interest payments on these debts can quickly eat away at your income, leaving you with less money to save for the future.

Make it a priority to pay off high-interest debts as quickly as possible. Consider using the debt snowball method, where you focus on paying off the smallest debts first, or the debt avalanche method, where you prioritize debts with the highest interest rates. By eliminating high-interest debt, you’ll free up more cash flow for retirement savings and reduce your overall financial stress.

Financial Goal Setting: Defining Your Retirement Vision

To stay motivated and on track with your retirement savings, it’s important to set clear financial goals. Think about the lifestyle you envision for yourself in retirement. Do you want to travel the world, pursue hobbies, or simply relax and enjoy your time? Once you have a vision for your retirement, you can estimate the amount of money you’ll need to save to achieve it.

Consider factors such as your desired retirement age, estimated living expenses, healthcare costs, and any other financial obligations you may have. By setting specific financial goals, you’ll have a target to aim for and a measurable way to track your progress.

3.Retirement Savings Vehicles and Strategies

Now that you have a clear understanding of your financial situation, it’s time to explore the various tools and strategies available to help you achieve your retirement goals. In this section, we’ll delve into the world of retirement savings vehicles, investment options, and strategies for maximizing your savings potential.

Employer-Sponsored Retirement Plans: Leveraging Matching Contributions

If your employer offers a retirement savings plan, such as a 401(k) or 403(b), it’s crucial to take full advantage of it. These plans allow you to contribute a portion of your pre-tax income to your retirement account, and in many cases, your employer will match a percentage of your contributions. This is essentially free money that can significantly accelerate your retirement savings.

Be sure to contribute enough to your employer’s plan to maximize the matching contribution. If you don’t, you’re leaving money on the table. Even if your employer doesn’t offer a match, contributing to their plan can still be a wise move, as it offers tax advantages and a convenient way to save for retirement.

Individual Retirement Accounts (IRAs): Choosing the Right Type for You

If an employer-sponsored retirement plan isn’t an option, or you’re seeking to enhance your existing retirement savings strategy, Individual Retirement Accounts (IRAs) offer a flexible and potentially lucrative avenue. These accounts come in two primary forms: Traditional and Roth, each with distinct tax advantages tailored to different financial situations.

- The Traditional IRA often allows for tax-deductible contributions, meaning you can reduce your taxable income in the year you contribute. Moreover, your investments grow tax-deferred, with taxes only becoming due upon withdrawal in retirement. This can be particularly advantageous if you anticipate being in a lower tax bracket during your retirement years.

- Conversely, contributions to a Roth IRA are made with after-tax dollars, but qualified withdrawals during retirement are entirely tax-free. This can be a powerful tool for long-term tax planning, especially if you expect your tax bracket to increase over time. Roth IRAs also offer more flexibility for early withdrawals of contributions (but not earnings) without incurring penalties.

Choosing the optimal IRA hinges on various factors, including your income level, current and projected tax brackets, and overall financial goals. Thorough research and comparison of the unique features and benefits of each type are crucial in aligning your retirement savings strategy with your individual circumstances. By understanding the nuances of Traditional and Roth IRAs, you can make an informed decision to maximize the growth potential of your retirement nest egg.

Investment Options: Build Your Own Portfolio

Having discussed retirement accounts, it’s time to consider how to invest in growing your net worth and generating passive income. Here are four common options:

- Stocks: Stocks represent ownership in a company. When you purchase a stock, you buy a small piece of that company, known as a share. Investing in stocks can be a powerful way to grow your net worth over time. Historically, stocks have provided higher returns compared to other types of investments, such as bonds or savings accounts, because companies can grow and increase their profits, which, in turn, increases the value of their stocks. However, stocks are typically more volatile than bonds, requiring a long-term strategy of purchasing and holding stocks regardless of market fluctuations. This approach leverages the market’s tendency to grow over time.

- Bonds: Conversely, bonds offer a more conservative investment option, often providing a reliable stream of income through interest payments. While their growth potential might be more modest compared to stocks, they can serve as a stabilizing force in your portfolio, particularly during turbulent market conditions.

- Index Funds: Index funds present a convenient and diversified way to invest in the broader market. These funds track specific market indices, such as the S&P 500, which includes 500 of the largest publicly traded companies in the US, spanning various industries. Index funds offer exposure to a wide range of stocks or bonds without the need for extensive research or stock-picking expertise.

- Real Estate: While real estate investment can be lucrative, it typically requires significant capital, expertise, and involves a certain degree of risk due to market fluctuations and potential maintenance costs.

Each asset class plays a distinct role, with some offering growth potential and others providing stability and income generation. It is crucial to do your own research and create a balanced approach that aligns with your risk tolerance and long-term financial goals.

Automated Savings Plans: Making Saving Effortless

One of the easiest and most effective ways to save for retirement is to set up an automated savings plan. This involves setting up automatic transfers from your checking account to your retirement account each month. By automating your savings, you’ll ensure that you’re consistently contributing to your retirement fund, even when you’re busy or tempted to spend your money elsewhere.

Increasing Your Income: Exploring Additional Sources of Revenue

In addition to saving diligently, consider exploring ways to increase your income. This could involve taking on a side hustle, freelancing, or starting a small business. The extra income you generate can be directed towards your retirement savings, allowing you to reach your financial goals faster.

4.Crafting and Adapting Your Retirement Plan

Retirement planning is not a one-and-done activity. As you progress through your 20s and beyond, your financial situation, goals, and risk tolerance may change. Therefore, it’s essential to regularly review and adjust your retirement plan to ensure it remains aligned with your evolving needs and circumstances.

Regular Reviews: Keeping Your Plan on Track

Make it a habit to review your retirement plan at least once a year. During these reviews, assess your progress towards your financial goals, re-evaluate your risk tolerance, and make any necessary adjustments to your investment portfolio. Consider factors such as:

- Income changes: If you’ve received a raise or promotion, increase your retirement contributions accordingly.

- Expense fluctuations: If your expenses have increased, adjust your budget and savings goals to accommodate them.

- Investment performance: If your investments aren’t performing as expected, consider rebalancing your portfolio or seeking professional advice.

- Life events: Major life events, such as marriage, buying a home, or starting a family, can significantly impact your financial situation and retirement goals. Adjust your plan accordingly to ensure it remains relevant and effective.

Seeking Professional Guidance: Personalized Advice for Your Unique Situation

While there’s a wealth of information available online about retirement planning, it’s often beneficial to seek professional guidance from trustworthy resources. Financial advisors are among the options available. They can assist you in creating a personalized retirement plan that is tailored to your specific needs and goals. They can also offer valuable insights into investment strategies, tax optimization, and risk management. Consider consulting a financial advisor if you:

- Feel overwhelmed by the complexity of retirement planning.

- Have specific questions or concerns about your financial situation.

- Want to ensure your investments are aligned with your risk tolerance and financial goals.

- Need help navigating complex financial products or strategies.

Adapting to Life Changes: Staying Flexible and Agile

Life is full of surprises, and your financial journey is no exception. Major life events, such as marriage, having children, or buying a home, can significantly impact your financial situation and retirement goals. It’s important to be flexible and adaptable, adjusting your retirement plan as needed to accommodate these changes.

For example, if you get married, you may need to coordinate your retirement savings with your spouse. If you have children, you may need to factor in the cost of their education and potentially adjust your retirement timeline. By staying flexible and proactive, you can ensure that your retirement plan remains relevant and effective throughout your life’s journey.

5.Overcoming Psychological Barriers and Common Misconceptions

Embarking on your retirement planning journey in your 20s is a wise decision, but it’s not uncommon to encounter psychological barriers or fall prey to common misconceptions that can hinder your progress. Let’s address some of these hurdles and debunk the myths that may be holding you back.

“I’m Too Young to Worry About Retirement”: The Importance of Starting Early

One of the most prevalent misconceptions among young adults is that retirement is something to worry about later in life. However, as we’ve discussed earlier, starting early is crucial for maximizing your retirement savings potential. The power of compound interest and the ability to navigate future uncertainties are compelling reasons to prioritize retirement planning in your 20s.

Remember, time is your greatest asset when it comes to saving for retirement. By starting early, you give your investments more time to grow and compound, ultimately leading to a larger nest egg in the long run. Don’t underestimate the impact of even small contributions made consistently over time.

“I Don’t Have Enough Money to Save”: Small Steps Lead to Big Results

Another common misconception is that you need a large income to start saving for retirement. However, even small contributions can make a significant difference over time. The key is to start small and gradually increase your savings as your income grows.

Consider these tips for saving on a tight budget:

- Track your expenses: Identify areas where you can cut back and redirect those funds towards your retirement savings.

- Automate your savings: Set up automatic transfers to your retirement account, so you’re saving consistently without even thinking about it.

- Start small: Even if you can only save $20 or $50 per month, it’s a step in the right direction. More importantly, you are cultivating healthy money management habits that will benefit you in the long term.

- Increase your savings gradually: As your income increases, gradually increase your retirement contributions.

- Look for ways to earn extra income: Consider taking on a side hustle or freelancing to boost your savings potential.

Remember, every dollar you save today is a step closer to achieving your retirement goals.

“Retirement Is Too Far Away”: The Long-Term Benefits of Saving

It’s easy to feel like retirement is a distant event, especially in your 20s. However, the sooner you start saving, the more time your money has to grow and compound. By the time you reach retirement age, your early contributions will have grown significantly, providing you with a comfortable and secure financial future.

Consider this: if you save $7,000 per year from age 25 to 35 and then stop, that money will continue to grow and could be worth over $780,000 by the time you retire at 65, assuming a 7% average annual return. This demonstrates the long-term benefits of saving early, even if you can’t sustain the same level of contributions throughout your working years.

And this is not just about retirement; the process is also rewarding. Through early planning and saving, you take a step to become more responsible for your own finances and more resilient to life’s challenges. Early retirement may be the destination, but what makes it more fascinating is the journey you are taking toward financial independence and security.

Conclusion

Embarking on your retirement planning journey in your 20s is a powerful step towards securing your financial future. By harnessing the power of compound interest, preparing for life’s uncertainties, and taking proactive steps to achieve financial freedom, you can set yourself up for a comfortable and fulfilling retirement.

Remember, retirement planning is not a one-size-fits-all endeavor. Your individual circumstances, goals, and risk tolerance will shape your unique path. However, the fundamental principles of starting early, saving consistently, and investing wisely remain constant.

Don’t let misconceptions or psychological barriers hold you back. Take action today, even if it’s a small step. Start by tracking your income and expenses, creating a budget, and exploring the various retirement savings options available to you. Seek professional guidance if needed, and remember to regularly review and adjust your plan as your life evolves.

By taking control of your financial future now, you can pave the way for a retirement filled with freedom, flexibility, and peace of mind. Remember, the journey of a thousand miles begins with a single step. Take that step today and start building the retirement you deserve.

For further information and resources on retirement planning, consider exploring the following:

- Your Money or Your Life: A transformative book that challenges conventional views on money and offers a path towards financial independence.

- WeFIRE app: An app that simplifies retirement planning and tracking, providing personalized insights and recommendations (Click here to learn more about WeFIRE).

The future is yours to create. Start planning for your retirement today and unlock the possibilities that await you.

Want to learn in a way that suits you? The “WeFIRE Library” offers a variety of resources to fit your learning style.

Personal Finance Tips for Financial Independence and Early Retirement

FIRE Budgeting 101: Your Essential Guide to Financial Independence

Master FIRE Money Management: Your Blueprint for Early Retirement

Start Early: How to Achieve Financial Independence While in College

WeFIRE Newsletter

A weekly roundup of money news, budgeting hacks, tax strategies, book reviews, and bursts of inspiration to support you on your path to financial independence.

Ellie Yan