If you’re on the FIRE journey, you probably know that one of the biggest financial hurdles is figuring out health insurance. If you’re not getting it through an employer, things can get pricey real fast. That’s where the Affordable Care Act (ACA) comes in. One of its key benefits is providing access to more affordable health coverage for those without employer-sponsored insurance. For many early retirees and freelancers, it’s been a game-changer.

As the ACA continues to shape how Americans secure insurance, it’s necessary to understand its nuances—who can benefit, how costs are managed, and what options are available for those without employer coverage. So, let’s dive in and break it down.

Eligibility

ACA is designed to include U.S. citizens and legal residents who are not incarcerated and live within a coverage area. Though the program primarily targets those without access to affordable employer-sponsored insurance, people at all income levels can sign up for coverage through Obamacare.

Government Subsidies under the ACA

The ACA includes financial assistance through two primary forms of subsidies to help reduce costs:

1. Premium Tax Credits: These directly lower monthly insurance payments based on household income, available to individuals and families earning between 100% and 400% of the federal poverty level.

2024 FPL is as follows:

| Household Size | 2024 Federal Poverty Level (FPL) | Income Range Eligible for Tax Credits |

| 1 person | $14,580 | $14,580~$58,320 |

| 2 people | $19,720 | $19,720~$78,880 |

| 3 people | $24,860 | $24,860~$99,440 |

| 4 people | $30,000 | $30,000~$120,000 |

| 5 people | $35,140 | $35,140~$140,560 |

Premium tax credits can lower your premiums for most Marketplace health plans. The amount of the tax credit you may receive depends on your income and the cost of plans in your area. For example, a couple without kids making $45,000 a year might pay about $490 a month for a Silver plan. Without the ACA, though, that could jump to almost $2,000 a month, which would be a big hit to their budget.

To qualify for these credits, you must buy insurance through the Marketplace, not have qualifying coverage through your employer, and meet certain income requirements based on the federal poverty level, adjusted for your region’s cost of living.

2.Cost-Sharing Reductions: Specifically assist with lowering out-of-pocket costs like deductibles and copayments for eligible enrollees.

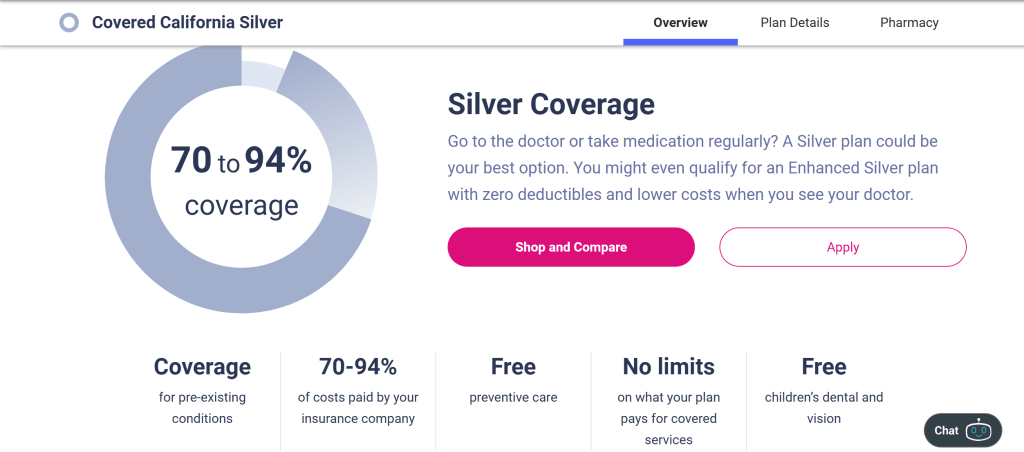

For example, John expects an annual income of $22,590 in 2025, or 150% of the poverty line. He enrolls in a silver plan, which could include a cost-sharing reduction, meaning he’ll pay less out-of-pocket for healthcare. This plan has an 94% actuarial value, which means the insurance company will cover 94% of his medical expenses on average, leaving him responsible for just 6%. This plan also has a much lower deductible of only $100.

Covered California Silver as an example

Diverse Insurance Types

The ACA marketplace typically offers four types of health insurance plans: Bronze, Silver, Gold, and Platinum. Each tier offers a different balance between monthly premiums and coverage, giving you the flexibility to select a plan that aligns with both your healthcare needs and your budget.

- Bronze Plan: Known for its affordability in terms of premiums, the Bronze plan typically covers about 60% of medical expenses. This plan requires higher out-of-pocket payments, making it ideal for those with limited budgets and minimal healthcare needs.

- Silver Plan: Offering a balanced approach, the Silver plan generally covers around 70% of medical costs. It is a popular choice due to its equilibrium between premiums and deductibles. Plus, Siver with extra savings are available to individuals or families whose income is between 100% and 250% of the federal poverty level when they enroll in a Silver plan.

- Gold Plan: Designed for individuals requiring more frequent medical services, the Gold plan provides approximately 80% coverage of expenses. It has lower deductibles compared to lower-tier plans, thereby offering more comprehensive coverage at a higher premium.

- Platinum Plan: At the top of the tier spectrum, the Platinum plan covers about 90% of healthcare costs. While it has the highest premiums, it offers the lowest deductibles, making it suitable for those needing extensive healthcare services.

Cost estimates when you get care

| Plan Category: | Premiums | Plan pays: | You pay: | Deductible is generally: |

| Bronze | Lowest | 60% | 40% | High |

| Silver | Lower | 70% | 30% | Moderate |

| Silver with extra savings | Moderate | 73-96% | 4-27%(Depends how much savings you qualify for) | Low |

| Gold | Higher | 80% | 20% | Low |

| Platinum | Highest | 90% | 10% | Low |

Coverage

Under the ACA, all marketplace plans are mandated to include a series of essential health benefits:

| Coverage Type | Description |

| Outpatient Services | Coverage includes doctor visits and preventive services, ensuring accessible routine care. |

| Hospitalization | Encompasses inpatient care, including surgery and overnight stays. |

| Prescription Drugs | Includes both generic and brand-name medications |

| Maternal and Child Health Care | Provides for pregnancy, childbirth, and newborn care, supporting family health needs. |

| Preventive Services | Addresses vaccinations and health screenings to maintain and monitor public health. |

| Mental Health and Substance Use Disorder Services | Offers counseling and treatment, integrating mental health care within overall health services. |

| Rehabilitative Services | Covers physical and occupational therapy, essential for recovery from health events. |

| Laboratory Services | Supports diagnostic procedures like blood and urine tests that are critical for health monitoring. |

Application Process

Purchasing ACA insurance involves:

- Visiting HealthCare.gov (Open Enrollment ends Jan 15) or your state’s marketplace site.

- Creating an account and providing personal details.

- Comparing available plans to assess coverage, premiums, and deductibles.

- Selecting a plan that aligns with your financial and healthcare needs.

- Completing registration and paying the initial premium.

Filing Taxes and Handling Adjustments

Beneficiaries of tax credits must report them using Form 1095-A when filing taxes. Changes in income can necessitate adjustments to the credits received, managed through IRS Form 8962 to ensure tax return accuracy and reconciliation.

What it means for FIRE group

Many individuals could only access decent health insurance through their employers. While there were a few plans available for individuals, they were often much more expensive and offered significantly less coverage. Although ACA health insurance plans can still be costly, they provide more options, especially for people without employer-backed options. Take, for example, a freelancer who shared her experience online. She has a Bronze plan, and thanks to health insurance subsidies, she was able to reduce her premium from $600 to $442.83, with a deductible of $6,200.

Another Internet post tells that a person who retired at 34 also uses an ACA plan. He pays $1,760 a month for a Platinum plan covering his family of three, as they don’t qualify for subsidies. While he feels that the $21,120 annual premium is excessive given their good health, he acknowledges the importance of supporting those less fortunate.

Many ACA plans are high-deductible health plans (HDHPs) paired with health savings accounts (HSAs), allowing pre-tax contributions for qualified medical expenses and savings for retirement health costs.

Compare ACA options and costs by state

If you’re considering early retirement and using the ACA for health insurance, it’s crucial to assess whether you live in a state with competitive premiums. Health insurance costs can vary significantly from state to state, and this can impact your overall retirement budget. For example, states like Iowa often have higher premiums and fewer affordable options. Some states have fewer insurance providers offering ACA plans, which could lead to higher costs or limited coverage options that may not meet your needs.

Some advocates of financial independence also ponder if they are in the best country for health insurance expenses, exploring options for more affordable coverage. We could discuss this topic in our future articles.

Last but not least, as the healthcare landscape keeps changing, it’s important to stay on top of the latest policies so you can make informed decisions.

WeFIRE Newsletter

A weekly roundup of money news, budgeting hacks, tax strategies, book reviews, and bursts of inspiration to support you on your path to financial independence.

Y H